The 2022-23 Budget has reiterated the government's commitment to boosting economic growth by seeking to increase public investment as a ratio of gross domestic product. In this context, R Nagaraj examines India’s current policy orientation and the outcomes of the recent investments in industry and infrastructure. He contends that the Budget's focus on industry seems to lack realistic proposals to reverse steeply falling output growth rates.

In 2018-19, India’s domestic output (GDP (gross domestic product)) in current US dollar terms is 2,701 billion, with a per capita income of US$ 1,997, and a poverty rate of 21.2 (International Monetary Fund (IMF), 2021). The annual real GDP growth rate has halved from 8.3% in 2016-17 to 4% in 2019-20, as per the National Accounts Statistics. Some estimates have also indicated that India's GDP growth rate became negative in 2019-20 – before the Covid-19 pandemic set in (Subramanian and Felman 2021). As the dispute concerning the official GDP estimates continues unabated, critics claim that the growth rates are probably lower than the official estimates, and the output deceleration perhaps spans most of the previous decade (Nagaraj 2020).

India’s output shrinkage

The Budget presented on 1 February forecasts India’s real (net of inflation) annual GDP to grow at 9.2% in the current year (2021-22) – the highest among the world’s large economies. However, the Budget fails to mention output contraction in the previous year (2020-21) – the worst among the world's large economies. Compared to the pre-pandemic year’s (2019-20) output level, the current year’s GDP will likely be marginally higher by 1.3% (Ministry of Statistics and Programme Implementation (MOSPI), 2022). If the adverse effect of the ongoing Omicron wave of Covid-19 is factored in, the forecasted increase may disappear. Thus, realistically, India has lost two years of output expansion, and per capita income in 2021-22 is likely to be lower by Rs. 844 (at constant 2011-12 prices), or by 0.8% than in 2019-20 (MOSPI, 2022).

The output shrinkage during the crisis meant a rise in unemployment, absolute poverty, and lost livelihoods. The informal or unorganised sector has borne the brunt of the pandemic and consequent lockdowns. For lack of up-to-date official data on employment and consumption, the 2021-22 Economic Survey seems to fail to offer a full and authentic picture of the economic devastation.

Abraham and Basole (2022) show a sharp rise in unemployment and deterioration in employment quality using the CMIE's (Centre for Monitoring the Indian Economy) pyramid database. Arguably, there are questions about the integrity of the database (Pais and Rawal 2021, Drèze and Somanchi 2021). However, the direction of change in employment reported in the CMIE data may be indisputable. If the critics' contentions have merit, the severity of the stress in the labour market is likely more, not less, than what Abraham and Basole (2022) report.

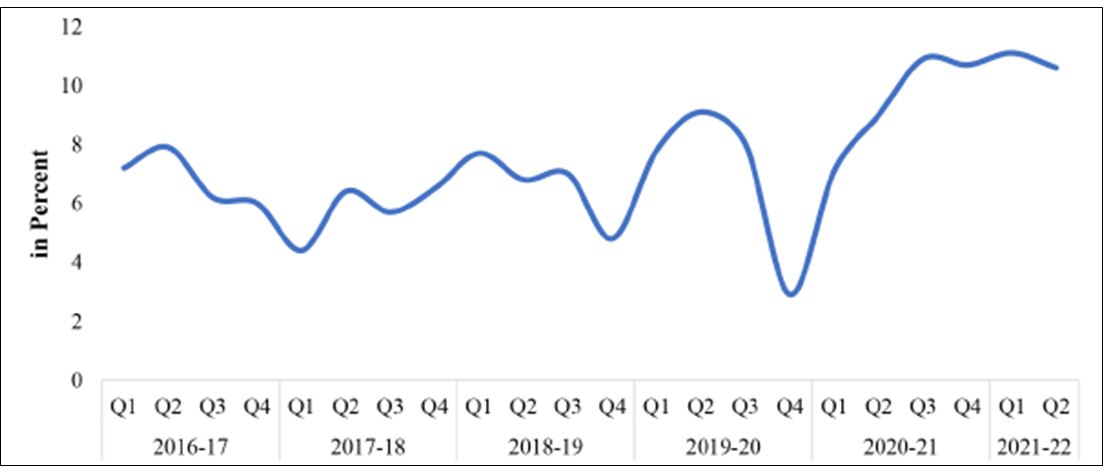

While the informal sector faced the brunt of the exogenous shocks, the 2021-22 Economic Survey shows that corporate profits boomed (Figure 1). India's current market capitalisation at 116% of GDP – in terms of the widely used measure of national wealth of equity holding – is higher that its long-term trend of 79% of GDP, and higher also than its previous peak in 2007 (the year before the Global Financial Crisis). Thus, juxtaposing the employment contraction with booming corporate profits, it seems reasonable to infer that economic inequality after the pandemic has widened, and recent research on trends in economic inequality has also documented this (Azad and Chakraborty 2022).

Figure 1. Net profit to sales ratio of listed manufacturing private companies

Source: Economic Survey 2021-22 (survey calculations based on data from the Reserve Bank of India (RBI)).

Current policy orientation

What could explain such an adverse outcome during the pandemic? No country escaped the devastation, but the variation in the impact of the shocks across countries suggests that policy response mattered. There are two reasons for India’s sharp economic contraction. To minimise the threat of the Virus, shutting down the country at the shortest notice of four hours caused immense disruption to production and people. It meant that millions of workers and their families, mostly in the informal sector, lost their jobs, livelihoods, and rented living spaces. The global index of the stringency of the lockdown captures well the severity of the ad hoc decision by placing India at the highest level of the index.

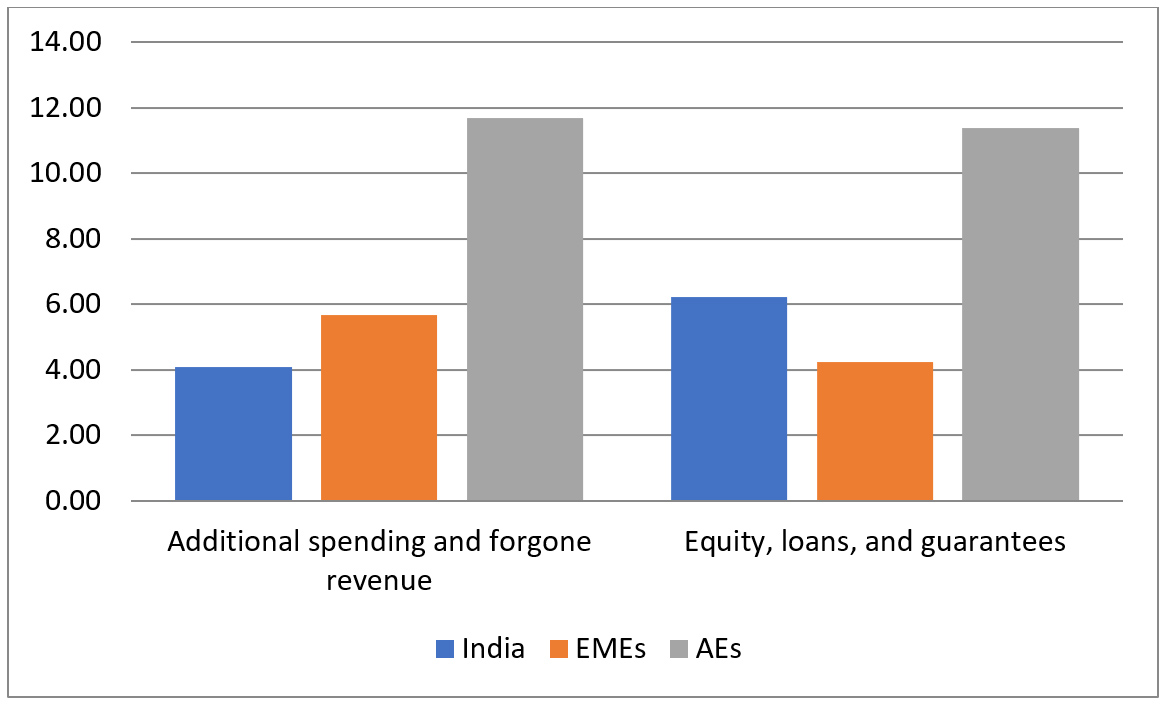

Two, the government’s efforts to mitigate the crisis were measly compared to most large economies. As per IMF data released in October 2021, fiscal support in India was lower than the average for the advanced economies (AEs), as well as for emerging market economies (EMEs) (Figure 2). For example, additional spending or revenue foregone in India since January 2020 was 4% of GDP, whereas it was close to 12% of GDP in advanced economies. India's response was greater in offering credit and loan guarantees (contingency funds), the utilisation of which was modest due to lack of demand. Moreover, that additional revenue provided for health during the pandemic was as meagre as 0.5% of GDP (IMF, 2021).

Figure 2. Fiscal support during Covid-19 since January 2020, as % of GDP

Source: IMF. Fiscal Monitor: Database of Country Fiscal Measures in Response to the COVID-19 Pandemic.

Why was India so stingy? Though the output growth was decelerating before the pandemic (as noted above), India’s macroeconomic situation was largely benign with low inflation, modest external imbalance, and tolerable fiscal deficit. Yet, India opted for supply-side reforms to strengthen long-term growth prospects – instead of stimulating aggregate demand by raising public spending in line with professional advice of economists with diverse analytical persuasions. The 2021-22 Economic Survey bears out the policy choice:

“…India’s response has been an emphasis on supply-side reforms rather than a total reliance on demand management. These supply-side reforms include deregulation of numerous sectors, simplification of processes, removal of legacy issues like ‘retrospective tax’, privatisation, production-linked incentives and so on… Even the sharp increase in capital spending by the Government can be seen both as demand and supply enhancing response as it creates infrastructure capacity for future growth.”

The outcome of the fiscally conservative response is evident (Table 1). Disaggregation of current GDP by sources of demand shows that private consumption, accounting for nearly 60% of domestic output, shrunk by three percentage points of GDP in 2021-22, compared to 2019-20. The step-up in government consumption mitigated the fall only to the extent of one percentage point of GDP. The share of fixed capital formation in GDP went up by one percentage point.

Table 1. Sources of aggregate demand (% of total)

|

Sources of demand |

2019-20 (1st revised estimates) |

2021-22 (advanced estimates) |

|

1. Total consumption |

71.1 |

69.7 |

|

1.1 Government consumption |

11.2 |

12.2 |

|

1.2 Private consumption |

60.5 |

57.5 |

|

2. Gross fixed capital formation |

28.8 |

29.6 |

|

3. Net exports |

(-) 2.5 |

(-) 3.0 |

|

4. GDP |

100 |

100 |

Source: 2021-22 Economic Survey.

The Budget's economic strategy

The Budget – barely referring to the ongoing Covid-19 pandemic and the suffering it has caused to the people of the country – reiterates the government's commitment to boosting economic growth by seeking to increase public investment as a ratio of GDP from 2.2% in the current year (2021-22) to 2.9%. Prima facie, such a strategy indicates a directional change in the theoretical underpinning of economic policy. Against the standard arguments of the ‘crowding-out’ effect of public investment, the Economic Survey has favoured the Keynesian logic of ‘crowding-in’ effect when real interest rates are low, and the economy is operating well below full capacity.

Figure 3 reports trends in fixed investment to GDP ratio and annual GDP growth rates for the last decade to provide perspective on this. The ratio declined from about 33% in 2012-13 to about 31% by 2019-20. However, the fall in the ratio would be far steeper if the data are extended backwards to 2008-09 when the figure touched 37%-38% of GDP and output was booming at 8-9% per year (Nagaraj 2020). Never in post-Independence history had India witnessed such a steep fall in aggregate investment rate for so long. Hence the changed reasoning underpinning the renewed emphasis on public investment-led economic revival, in principle, stands to reason.

Figure 3. GDP growth rate and fixed investment ratio

Source: National Account Statistics (2021).

But there lies the rub. Is it the right moment to prioritise investment when the country faces massive job loss, livelihoods, and a rise in absolute poverty? The government seems to underplay the gravity of human suffering by only looking at the broken instruments of official statistics. But the picture that emerges from credible independent voices seems fairly unanimous and the evidence appears grave. As private consumption's share in GDP declined, sensible policy response demands the immediate restoration of employment and earnings directly through employment generation or income support programmes – as in many economies such as the US or Canada. The proposed investment demand will indirectly create jobs, but it may take a while to materialise, given the roundabout nature of fixed investment. How much employment these investments generate will depend on the labour intensity of the investments. Further, given the high level of industrial import in domestic manufacturing, employment generation prospects would get dented to that extent.

On the practical side, whether the budgetary arithmetic really supports the investment agenda seems questionable. First, contrary to the Finance Minister's claim, the proposed rise in public investment's share in the Budget is similar to what was presented last year. As per my calculations, the increase in public investment accounted for barely 0.2% of GDP. Knowledgeable commentators have contended that the proposed 35.4% rise in public investment expenditure over the last year may be a statistical mirage.

Investment in industry and infrastructure

The Budget statement goes at length to describe government initiatives such as PM Gati Shakti, Make in India, Atmanirbhar Bharat (self-reliant India), and so on. But it fails to provide quantitative details of achievements of these initiatives so far and how the proposed investment hopes to reverse the declining aggregate investment rate described above.

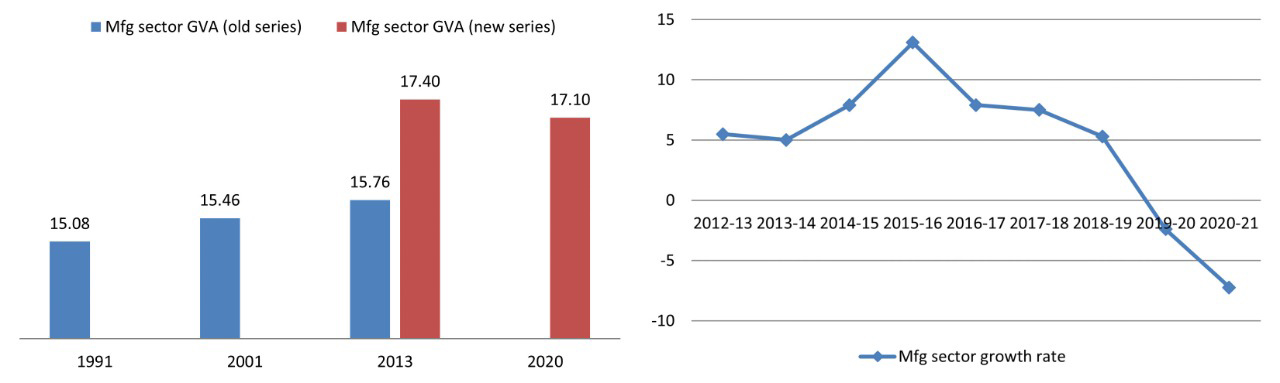

The ‘Make in India’ initiative, for instance, was launched in 2014-15 to raise the manufacturing sector's share in GDP to 25% and create 100 million additional jobs in the industry by 2022. Despite the hype, little came out it. The manufacturing sector's share in GDP continues to languish at around 17% as of 2019-20 (Figure 4). The manufacturing sector annual output growth rate at constant prices sharply plummeted from 13.1% in 2015-16 to -7.2% in 2020-21. What could explain such an adverse outcome, and how does the government hopes to reverse the declining trend through the proposed public investments? There are few answers.

Figure 4. Manufacturing sector performance – share in GDP (left panel) and growth rate (right panel)

Source: National Accounts Statistics; 2021-22 Economic Survey.

The government frittered away valuable policy space in seeking to improve India's global rank in the World Bank's Ease of Doing Business (EDB) index, believing that the improved ranking will raise investment inflows. Indeed, EDB rank increased impressively, from 142 in 2014 to 63 in 2019-20. But investments failed to materialise. Why? The EDB index is a spurious measure with little analytical and predictive value. Embarrassingly for the government, the World Bank scrapped the index last year as its methodology came under a cloud for being politically motivated. Yet, surprisingly, the Budget statement eloquently vouches for pressing ahead with measures to make business easier by deregulation of industrial laws without pausing to take stock of what went wrong with the Make in India campaign.

In 2020, as part of Atmanirbhar Bharat initiative, the government introduced a 'Production-linked Incentive Scheme’ (PLI) for three industries. The scheme was extended to 10 more industries with an outlay of Rs. 1.97 lakh crore in 2021 for five years. The Economic Survey claims large numbers of investment approvals but offers no information on the outcome of the effort in terms of investment, output, and exports.

A few years before launching the PLI, the government was pursuing a "phased manufacturing programme” (PMP); with a conscious effort to indigenise mobile phones production whose domestic demand was rising rapidly. The Economic Survey claims the success of the mobile phone-assembly industry, which reportedly formed the basis for seeding the PLI scheme. However, this effort has shown modest success, contrary to official claims (Iyer 2021).

In May 2020, amid scarcity of critical pharmaceutical inputs that were immediately required for fighting the pandemic, India launched Atmanirbhar Bharat, to expand domestic production of such intermediate inputs. India raised tariffs on Chinese imports and imposed various non-tariff barriers in response. Over a year on, positive outcomes are hard to come by. On the contrary, India’s trade deficit on China has gone up – from US$ 39.8 billion in 2020 to US$ 64.5 billion in 2021 by Indian trade statistics, from US$ 45.8 billion in 2020 to US$ 69.4 billion in 2021 as per China’s trade statistics (Table 2). The deficit would be bigger if net imports from China included Hong Kong.

Table 2a. India-China trade (as per India’s estimates, in billion US$)

|

Year |

India’s exports |

India’s imports |

India’s trade deficit |

|

2018 |

16.5 |

73.9 |

57.4 |

|

2019 |

17.1 |

68.4 |

51.3 |

|

2020 |

19 |

58.7 |

39.7 |

|

2021 |

23 |

87.5 |

64.5 |

Source: Dhar (2022); Department of Commerce, India.

Table 2b. India-China trade (as per China’s estimates, in billion US$)

|

Year |

China’s exports |

China’s imports |

India’s trade deficit |

|

2018 |

76.7 |

18.8 |

57.9 |

|

2019 |

74.8 |

18 |

56.8 |

|

2020 |

66.7 |

20.9 |

45.8 |

|

2021 |

97.5 |

28.1 |

69.4 |

While advocating a public investment-led growth strategy may be welcome in principle, it needs to be backed it up sectoral and industry-specific policies and programmes, and supply of long-term credit under the rubric of an industrial policy. The 2008 Global Financial Crisis and, more recently, the Covid-19 pandemic, have culminated in the reimagining of industrial policy across the world amid weakening political commitment to free trade.

Conclusion

India has lost two precious years of output expansion due to the pandemic and the world's most stringent lockdown imposed in response. Most economists have endorsed boosting public spending support aggregate demand and prevent employment loss. Perceiving an opportunity in the distressed situation – perhaps following the adage, never waste a crisis – India has prioritised supply-side measures. Hence, not surprisingly, India’s output loss seems quite adverse – with a rise in unemployment (and deteriorating quality), and poverty and inequality. The scars of the pandemic are however barely visible in metrics used in the Economic Survey for lack of official data.

Against the above, the Budget aims to raise public investment's share in GDP seems to ring hollow, as it sticks to the fiscal consolidation roadmap laid out last year. Moreover, the underlying budgetary arithmetic appears to lack credibility given the absence of the details.

More seriously, is it the right moment to raise the investment rate, ignoring the immediate economic distress? Instead of increasing, the Budget has cut the allocation for the demand-driven MNREGA (Mahatma Gandhi National Rural Employment Guarantee Act)1 scheme, perhaps suggesting apathy towards the most vulnerable sections.

The Budget's focus on industry seems to lack realistic proposals to reverse steeply falling output growth rates, and the spectre of India becoming an import-dependent economy on China – with potentially profound strategic consequences.

Note:

- MNREGA offers a guarantee of 100 days of wage-employment in a year to a rural household whose adult members are willing to do unskilled manual work at the prescribed minimum wage.

Further Reading

- Abraham, R and A Basole (2022), ‘Covid-19 and the Informalisation of India’s Salaried Workers’, The India Forum, 7 January.

- Azad, R and S Chakraborty (2022), ‘A Tale of Two India’, The India Forum, 4 February.

- Dhar, B (2022), ‘Addressing dependence on China as trade rises’, The New Indian Express, 24 January.

- Drèze, J and A Somanchi (2021), ‘New barometer of India’s economy fails to reflect deprivations of poor households’, The Economic Times, 21 June.

- International Monetary Fund (2021), ‘IMF Country Reports 21/230’, Report.

- Iyer, C (2021), ‘Mobile Phone manufacturing in India: A study of few characteristics’, CDS Working Paper 502.

- Ministry of Statistics and Programme Implementation (2022), ‘Press note on first advance estimates of national income 2021-22’, National Statistical Office, Government of India.

- Nagaraj, R (2020), ‘Understanding India’s Economic Slowdown’, The India Forum, 7 February.

- Pais, J and V Rawal (2021), ‘CMIE’s Consumer Pyramids Household Surveys: An Assessment’, The India Forum, 3 September.

- Subramanian, A and J Felman (2021), ‘Peering Back to Look Forward: Measurement to Prognosis’, IGIDR Macro Conference 2021.

Social media is bold.

Social media is young.

Social media raises questions.

Social media is not satisfied with an answer.

Social media looks at the big picture.

Social media is interested in every detail.

social media is curious.

Social media is free.

Social media is irreplaceable.

But never irrelevant.

Social media is you.

(With input from news agency language)

If you like this story, share it with a friend!

We are a non-profit organization. Help us financially to keep our journalism free from government and corporate pressure

0 Comments